|

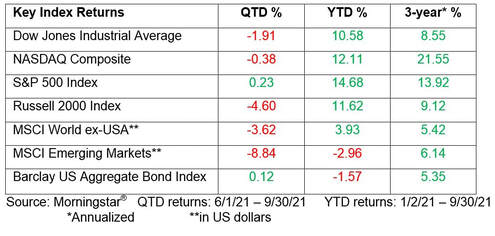

Dear Friends, The Fall season is upon us – thankfully. Football and cooler temperatures! Life is good. Hopefully this note finds you and your family well, rested from your summer travels and feeling good. ZOOM Webinars for Clients Last month’s presentation on “Estate Planning in the COVID Era” is available for replay. The broadcast can be found in the Media & Posts tab on our website www.realityfinancialplanning.com. When it comes to planning for a safe and secure retirement, long-term care (LTC) can be a confusing and unaddressed challenge to many families’ financial security. Some of the hesitancy can be pinned to human nature - we don’t want to think about the unpleasant possibility of needing help with caring for ourselves (i.e., feeding, bathing, using the bathroom). Some might think it won’t happen to them; while others would rather “deal with it later”. So, mark your calendars for Thursday, October 28, 2021, at 5:00, to join our ZOOM webinar on “Financial Planning for Long-Term Care”. We will provide ideas to start the LTC discussion and things you may want to think about when preparing for the potential need for, costs, misconceptions, and other LTC considerations. If you are interested in attending, please email us at [email protected] and John will send you the ZOOM meeting details. Will Social Security Go Bust? You may have read that the Social Security Trust Fund is due to be depleted in 2033, a year earlier than previous projections. This sounds alarming, except for several caveats. First, the projected date of depletion has been in the 2035 range for the past decade, so this shift is really nothing new—or particularly alarming. The immediate cause of the shortened timeline is, of course, the slowdown of economic activity due to COVID. The Social Security Trust Fund collects payments out of the wages of millions of American workers; when those workers are laid off or otherwise unable to collect paychecks, then the Trust Fund is unable to collect its share of those paychecks. In its annual report, the Social Security Administration says that it is projecting that employment and wages will gradually rise to full recovery by 2023, but that the level of worker productivity and U.S. Gross Domestic Product will be permanently lowered by 1%. That permanent decline is not a consensus view of economists and should be viewed with caution. In addition, the report projects that there will be a higher mortality for persons aged 15 and older through 2023—meaning, once again, fewer workers collecting paychecks. But the COVID mortality figures are much lower for working individuals and much higher for the people who would actually collect old age benefits—and there is no provision in the report accounting for the death of more than 200,000 Americans who were collecting Social Security checks. In fact, the report notes that the trust fund’s reserves, at $2.9 trillion, were $11 billion higher this year than they had been the previous year—and the pool that pays out retirement income increased by $7.4 billion. A chart shows that the Old Age and Survivor Insurance pool took in $968.3 billion in 2020 and paid out just $961 billion. The gloomy projection reported in the press is based on “less revenue anticipated in the near term,” meaning, once again, those projections of permanently lower economic activity, and the death of many more workers, due to COVID. Of course, most people—including reporters—don’t understand how the Trust Fund works. The Social Security system collects its revenues from those worker paychecks (and employer matches), and then turns around and pays that money out to Social Security beneficiaries. The trust fund currently, as mentioned, has $2.9 trillion in assets—much of it in government securities. That pool of money pays out any annual shortfall between the amounts collected and the benefits—and the fact that it increased this past year suggests that it didn’t have to reach into its pocket, at all, for the past 12 months. If, and when, the Trust Fund does run out of money, the Social Security Administration would simply pay out the monies collected without a supplement—and if nothing is done by 2033, that is projected to be 78% of the benefits paid out today—remembering, of course, that it was enough to pay out 100% in the past year. The important thing to note is that 78% is not zero; it’s more than three-quarters of the expected benefits. And of course, once again, this is based on a lot of assumptions, including the idea that few Americans will continue working after they receive their benefits, that the economy will never fully recover from COVID, and that pandemic mortality will be evenly distributed between the young and the old. Finally, does anybody really think that Congress would allow the cohort of voters currently receiving Social Security benefits to take a sudden 22% haircut in that portion of their retirement income? 69.1 million people currently receive benefits, and one can guess that many of them are motivated voters. Expect some age/benefit tweaks, and some higher payroll taxes, long before you see any reductions in the Social Security income received by elderly Americans. Market Perspectives January was the last time the S&P 500 index finished the month in the red – down 1.1%. As we enter the fall months, we know that September has historically been the weakest month for stocks and last month was no exception. Reviewing monthly S&P 500 data back to 1970, September is the only month that averages negative returns; this past month the S&P 500 was down 4.76%. Is it rising COVID cases and the possible economic impact, are investors eyeing an eventual Fed taper, are looming tax changes and budget quarrels affecting behavior, or is the ghost of Septembers past just influencing sentiment? If you look at the charts for the past year, the S&P 500 had not experienced a 5% decline. In fact, every time we approach the 50-day moving averages, buyers have stepped in.  Thus far, it has only been a minor setback. But, please keep in mind, the S&P 500 is up 28% over the past year, which is on top of the sharp recovery that completely erased the losses sparked by the early days of COVID pandemic.

We hate to say we are due for the pullback, but anticipating a correction is rarely a profitable strategy. Meanwhile the fundamentals that have underpinned stocks remains in place.

Conclusion As always, thank you for the trust and confidence you place in us. It is something we never take for granted and sincerely appreciate. Please do not hesitate to reach out whenever you have questions, concerns or may be of service to you. Sincerely, Joe Downs, CFP® & John Cunningham, CFP® Comments are closed.

|